by John Harris, Director & Idette Elizondo, Manager

HFM Blog

November 2015

Open PDF file >

BPCI Year 1: Lessons and Opportunities

Results have come in for the first performance year of Medicare’s Bundled Payment for Care Improvement (BPCI) program. Providers are taking stock of successes and identifying areas for improvement. (They are not yet taking stock of losses, given that downside risk was waived in 2014.)

Key Observations

All organizations for which we have data reduced costs below target, generating savings for Medicare, but not all covered the added BPCI program expenses. The following trends are evident in their experiences to date.

Care redesign is happening. These organizations have successfully implemented redesigned care protocols in accordance with Centers for Medicare & Medicaid Services (CMS) requirements. Protocols for medical and surgical bundles appear quite different from one another, with bundles for medical diagnoses, such as congestive heart failure, requiring more intensive interventions. Protocols now extend to settings beyond discharge, and analysis of CMS claims data verifies that participants have shifted care to lower-cost settings such as home health care.

Alignment with post-acute providers is working. Most of the organizations in BPCI that we looked at are hospitals focusing on post-acute costs, which typically represent the largest opportunity to generate savings. This focus has resulted in the creation of formal partnerships with post-acute care providers. Hospitals have been successful in shifting care to lower-cost settings after discharge, with some reducing length of stay in skilled nursing facilities. Regular meetings with post-acute care providers have been key to engaging them and changing practice patterns.

Patient care is improving. All of the organizations have seen improvements in a variety of clinical indicators. Some have reduced readmission rates by up to 50 percent from the prior year. One hospital participating in a joint replacement bundle has increased the percentage of readmissions that return to the hospital rather than go elsewhere from 30 to 100 percent, allowing the hospital’s clinical team to more closely monitor patients and identify new ways to decrease readmissions.

Medicare costs are down; internal cost savings vary. All of the organizations have seen a decline in average cost per episode, as well as a change in the distribution of costs over an episode (e.g., a higher proportion of the total going to home health compared with skilled nursing).

Internal cost savings are more variable, depending on how much the organization previously has done to reduce cost. Physicians have not yet focused on internal costs, but may start to do so when they see the additional opportunity to share in savings.

Gainsharing can be meaningful. Among physicians who are participating in gainsharing, incentive payments account for as much as 10 percent of compensation.

Future Opportunities

BPCI participants should continue to focus on engaging physician and post-acute care partners, given the significant influence of those entities on the success or failure of care bundles.

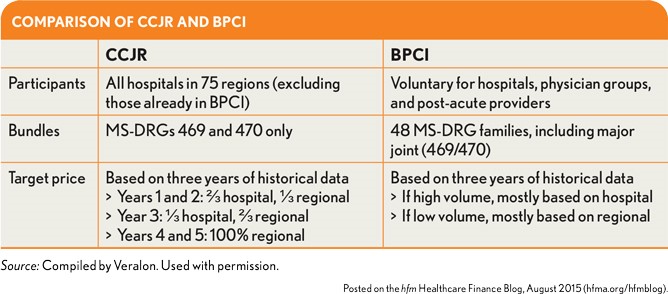

CMS must like the results it is seeing from BPCI. The agency has proposed the Comprehensive Care for Joint Replacement (CCJR) program (see exhibit above), which is scheduled to launch in January 2016 and will require all hospitals in 75 regions to accept a bundled payment for hip and knee replacements during a five-year period.

CCJR participants can draw on the experience of BPCI participants, given the similarities between the programs.